What does the real estate market need after years of being first overheated during the COVID-19 housing boom and then effectively frozen by the high mortgage rates that followed? A run at plain old room temperature.

The market appeared to be heading in that more typical direction in the week ending Jan. 20.

“This past week, the housing market showed the early signs of a return to normal, with slowing median listing price growth, a growing inventory of homes for sale, and mortgage rates which have fallen more than a percentage point from their recent peak,” says Realtor.com® economic dMortgage rates for a 30-year fixed-rate home loan ticked up to an average of 6.69% for the week ending Jan. 25, according to the latest Freddie Mac data. Yet that figure “has remained within a very narrow range over the last month,” says Freddie Mac Chief Economist Sam Khater. (Last week’s rate averaged 6.60%.)

With nearly two months of winter left, will buyers and sellers brave the cold to take advantage of a surprisingly temperate market?

We’ll explain what the latest housing market data means for anyone tempted to get off the sidelines and into the real estate game in the latest installment of “How’s the Housing Market This Week?”

Where mortgage rates might be headed

All market watchers will be tuned in to see what the Fed does at its next meeting at the end of this month. Why? Because the Fed’s relentless raising of interest rates to tame ballooning inflation is what essentially triggered mortgage interest rates to double over the past two years.

Now, the Fed is poised to cut rates this year as inflation falls closer to its 2% goal. This will likely put pressure on mortgage rates to fall. However, those eagerly anticipated rate cuts aren’t likely until the spring or summer.

“Looking forward, recent employment and inflation data came in relatively strong, suggesting that the Fed will likely opt to hold the policy rate steady in their upcoming meeting,” explains Speianu. “Continued progress toward the 2% inflation rate target is expected, and this will eventually improve housing market conditions in 2024.”

Home prices finally budge

While the median home list price rose by 1.9% for the week ending Jan. 20 compared with the prior year, the growth in prices declined from the previous week. (The median listing hit $410,000 in December.)

This is good news for buyers who have been grappling with the high price hikes over the past few years. While prices are still rising, they’re doing so much more slowly than the double-digit price hikes experienced during the pandemic.

“Listing price growth appears to be cooling after reaching a 35-week high during the week ending Jan. 6,” says Speianu. “If this trend continues, homebuyers stand to benefit from a decline in mortgage rates and slower, moderate home price appreciation.”

The ongoing inventory uptick

The new year has brought a welcome trove of new homes for sale, which were a rare sight during a considerable stretch of last year.

New listings were up for the week ending Jan. 20 by 3.4% from one year ago. While this growth is less than last week’s 7% growth rate, “newly listed homes continue to rise above last year’s levels for the 13th week in a row,” notes Speianu.

Active listings (a measure of both old and new homes for sale) grew by 8.6% for the week ending Jan. 20 compared with the year prior. That marked an 11-week streak of annual growth.

And in promising news for buyers, there’s “no sign yet of a slowdown as growth in inventory,” says Speianu.

The case for not waiting for the spring market

Some buyers and sellers might be tempted to hold out for the busy spring housing market to kick into gear before getting off the proverbial bench.

Yet many home shoppers are already in the game—and snapping up properties.

The typical home flew off the listing pages four days faster in the week ending Jan. 20 than in the same period last year. (In December, homes spent an average of 61 days on the market.)

Chalk the faster pace of sales up to the influx of fresh listings and lower mortgage rates in a market filled with hungry buyers ready to pounce once they find homes they can afford.

Buyers ready to make the move and sellers who need another home to move to might want to act fast before prices—and the competition—rise even more.

“This year, the first few weeks of January are shaping up to look more like slower seasonal growth seen in the years 2017 to 2020, where listing prices begin to pick up later in February,” says Speianu.

Margaret Heidenry is a writer living in Brooklyn, NY. Her work has appeared in the New York Times Magazine, Vanity Fair, and Boston Magazine.

http://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.png00Phil Whiteheadhttp://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.pngPhil Whitehead2024-02-04 11:23:412024-02-04 11:24:09The Housing Market Just Showed a Sudden, Miraculous ‘Return to Normal’—Take a Look

Homeowners often love to humble-brag about various aspects of their abode, from the size of their primary suite to just how many cars can fit in their garage.

But the latest boast has nothing to do with square footage and everything to do with numbers—today’s homeowners like to boast their look-how-lucky-I-got low mortgage rates.

If you missed out on the friendly mortgage rates your friends or family nailed down buying homes during the COVID-19 pandemic, join the club. Homebuyers today are feeling mortgage envy in a big way as interest rates surge to new heights.

Here’s how to deal with those who feel the need to flaunt their low mortgage rates (and how to get a rate you’ll want to show off).

Mortgage rate envy, explained

Many lucky homeowners snagged a rate of 2.65% in January 2021, but hearing about it will likely grate on the nerves of today’s buyers facing a current 23-year high of 7.57%.

Jealousy is human nature, after all.

“Envy often stems from issues related to self-worth, identity, and unmet desires or needs,” says William Schroeder, counselor and co-owner at Just Mind in Austin, TX. “How mortgage envy relates to this situation is pretty clear: The person who gets the house at a better deal is perceived as to be envied.”

In other words, your needs remain unmet while someone else’s are fulfilled.

Owners and buyers are green-ish with envy

No one will throw shade if you feel bitter that your pals scooped up a 3.5% interest rate just last year when you’re looking down the barrel at a rate twice as high.

“I absolutely have mortgage rate envy for the people who bought homes anytime before 2022,” says Carter Seuthe, CEO of Credit Summit. Seuthe’s been house shopping for a year and, to make matters worse, was outbid on two offers.

“It is easy to allow situations like this to go into a ‘compare and despair’ cycle,” says Schroeder. “We have such an abundance of data and social media tools that highlight obvious points of comparison.”

Jake Hill, CEO of DebtHammer, was on the compare and despair ride when he first learned of his friend’s variable rate.

“The introductory rate was so much lower than mine, and I almost felt like I had made a mistake choosing a fixed-rate loan,” says Hill. “However, I reminded myself that, in time, that variable rate will balance out, and their mortgage choice won’t look like such a steal.”

How to deal with a mortgage bragger

Feeling jealous of someone else’s good fortune is one thing, but when someone knows you’re house shopping and goes on (and on) about their low interest rate, it rubs salt into the wound.

“Normally, when this comes up, it’s a sign a person is looking for confirmation of self-worth,” says Schroeder. “Very often, this is rooted in an insecurity of some sort as they are trying to boost themselves up and show some superiority.”

Humble braggers might expect a high-five for their perceived shrewd wisdom and perfect timing in conquering the housing market. But it’s OK if you can barely muster up enthusiasm to congratulate them.

And Schroeder notes that not all boasting comes from a negative place. Instead, the need to show prowess might be cultural.

“Maybe someone comes from a specific background that rewards financial savvy or thrift,” says Schroeder.

How lenders deal with mortgage rate envy

So, who hears about mortgage rate envy the most? Mortgage lenders!

“We often find clients coming to us with stories of how their friends or family managed to secure lower interest rates on their mortgages,” says Alex Shekhtman, CEO and founder of LBC Mortgage in Los Angeles.

He recently had a client who was disheartened when she found out a relative had snagged a lower interest rate for their new home.

“She felt like she was missing out on something great,” says Shekhtman.

Tips to get a lower interest rate

The good news for buyers with mortgage rate envy is that lenders might be able to turn those understandably sour grapes into something less bitter.

Shekhtman’s client worked to improve her financial profile and qualified for a better rate. Here are his suggestions on how you can nab a lower interest rate.

Boost your credit score: “Lenders often reward borrowers with higher credit scores by offering more favorable rates,” says Shekhtman.

Compare multiple mortgage rate offers: “By comparing multiple offers, you increase your chances of finding a rate that aligns with your financial goals,” explains Shekhtman.

Make a bigger down payment: Putting down a chunk of change might be rewarded with a lower interest rate by a lender. Also, some FHA programs offer rates that are lower than conventional loans and with only a 3.5% down payment.

Buy mortgage points: “Some lenders let you buy mortgage points, which means you prepay interest upfront in exchange for a lower interest rate for the whole loan term,” says Shekhtman. Do the math and determine if buying points makes sense in the long run.

It’s OK to (quietly) have mortgage rate pride

John Kennelly, founder of F3 Collective in Dallas, refinanced his original 4.25% mortgage from 2019 to a 3% rate in August 2020.

But he doesn’t shout it from the rooftops.

“We do our best not to reveal our rate to friends buying a home right now,” says Kennelly. “We feel for friends who need to buy a new home right now.”

Though Kennelly does admit a private sense of pride: “My wife and I always share a wry smile for how lucky we are to have capitalized on the low rates during COVID.”

Lisa Marie Conklin knows a little something about moving. She’s moved eight times in the past 10 years but currently calls Baltimore home. She writes for Reader’s Digest, Family Handyman, The Healthy, Taste of Home, and MSN.

http://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.png00Phil Whiteheadhttp://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.pngPhil Whitehead2023-12-29 18:37:202023-12-29 18:37:22Got Mortgage Rate Resentment? Here’s How To Cope (and Get a Lower Rate)

The top emerging housing markets in America this fall have one key thing in common: They’re generally places where buyers can still find an affordably priced home.

“These areas are relatively inexpensive,” says Hannah Jones, a senior economic research analyst at Realtor.com. “Inflation remains high, home prices are high, mortgage rates are high, so buyers are being hit from every angle right now. … For buyers who do need to purchase a home, it’s important that they can find one where the monthly payments are going to be reasonable.”

The index identified the top markets for both buyers and investors out of the 300 largest metropolitan areas. It looked at metros with strong housing demand based on page views of local listings, the number of homes for sale, property taxes, and median days homes sit on the market before a sale. It also factored in metros with robust economies, lots of well-paying jobs, a good quality of life, and desirable amenities such as lots of small businesses and reasonable commutes to work. (Metros include the main city and surrounding towns, suburbs, and smaller urban areas.)

With home prices back on the rise and mortgage rates nearing 8%, the budgets of many buyers have been stretched beyond their breaking points. Nationally, home prices were about 40% higher and the typical mortgage payment was 114% larger in September than just four years earlier. That’s led some buyers to seek out cheaper places to live.

“Wage growth has not kept up with inflation,” says Jones. “Homes have to be low-priced for monthly mortgage payments to be reasonable.”

Nearly all of the top 20 emerging housing markets this fall either boast low home prices or are cheaper alternatives to pricier nearby cities. Just over half of the markets were in the Midwest, with three of the top five in Indiana.

Prices in these markets, however, are rising quickly. They shot up an average of 19% year over year in September compared with 9.5% nationally. Since the COVID-19 pandemic, prices shot up 69% compared with 47% nationally.

“Many of these areas didn’t see some of the early pandemic price surges,” says Jones. “These more affordable areas are pulling in interest from out-of-area buyers. It’s highly possible that they have higher incomes and therefore may be willing to prop up that price growth, because homes are still relatively affordable compared to the U.S. as a whole.”

Buyers can still find homes priced below $200K in Topeka

In Topeka, buyers can still find a three-bedroom, two-bathroom home in the city limits for less than $200,000 if they don’t mind putting in some work, says local real estate agent Patrick Moore, of Keller Williams One Legacy Partners.

Larger, move-in ready homes in desirable suburbs are priced a bit higher, in the mid-$200,000s.

“We see a higher number of people relocating here from the West Coast and other more expensive areas,” he says. “People have figured out that living in our area is way, way cheaper. But there’s still job opportunities here, and there’s less traffic.”

Homes also cost about 40% less than in Kansas City, MO, about an hour west of Topeka.

However, the housing market is much more competitive today than it was before the pandemic. The median home price is about $100,000 more than it was in September 2019. And while the number of homes for sale has been steadily increasing over the past year, there are still about 50% fewer properties than there were a year earlier.

“It’s still a pretty hot seller’s market in our area,” says Moore.

Home prices are relative

Not every home on the list was cheap. A quarter of the top 20 emerging markets had prices that were more than the national median list price of $429,500 in September.

In New Hampshire, Manchester (No. 7) and Concord (No. 8) both had prices above $500,000. But homes in these metros were a steal compared with Boston, about an hour southeast of the cities, where homes cost a median of $849,000. About 90% of views on Concord home listings were from out-of-town home seekers.

Priced-out buyers were also drawn to Worcester, MA (No. 2o). The metro’s median list price was $490,000—more than $350,000 less than in Boston, about an hour’s drive to the east.

The one outlier on the list was the Santa Maria metro, about three hours north of Los Angeles along the coast of Southern California. The wealthy area, which includes tony Santa Barbara, attracts interest from international buyers.

“Buyers in Santa Barbara may not be as impacted by the affordability constraints,” says Jones. “They may not be as worried about mortgage rates because it’s more likely they’ll be paying in cash or putting down a larger down payment.”

Clare Trapasso is the executive news editor of Realtor.com. She was previously a reporter for the Associated Press, the New York Daily News, and a Financial Times publication. She also taught journalism courses at several New York City colleges. Email clare.trapasso@realtor.com or follow @claretrap on X (formerly Twitter).

Everyone seems to know someone who knows someone who hit the real estate jackpot: lucky folks who bought a home for a relative pittance back when prices were low and then sold it a few years later for a windfall.

So where are the next hot spots to buy a home?

While it’s nearly impossible to time the housing market, certain parts of the country are expected to fare better than others this coming year, according to the Realtor.com® 2024 forecast.

In this forecast, Realtor.com identified the real estate markets where home sales prices are anticipated to grow, even as they dip nationally. The number of existing-home sales in these places is also expected to surge, despite remaining mostly flat in much of the rest of the country.

The top 10 markets in 2024 “have been more steady,” says Realtor.com Chief Economist Danielle Hale. “They haven’t seen the big price and sales booms we’ve seen in other parts of the country, which helps them to stand out now.”

The Realtor.com economics team predicted home sales prices as well as the number of existing-home sales, which excluded new construction, in the 100 largest metropolitan areas.

Ironically, two of the nation’s most expensive states claimed seven of the top 10 spots. Half were on the West Coast, in notoriously pricey California, with two in Massachusetts.

That might come as a surprise as homebuyers have increasingly been seeking out pockets of affordability as mortgage rates spiked and home prices have remained historically high. Those high costs resulted in a rough year for the Golden State housing market. As it became even more unaffordable to purchase a home in California, prices slumped in many areas and sales dried up.

Many of these Southern California markets are expected to rebound in 2024. As mortgage rates are predicted to fall in the year ahead, it will bring more buyers into the market who are expected to bid up prices. Equally important will be the additional sellers who are likelier to put their homes up for sale, boosting inventory, as they become more confident they can find new ones. That will result in more sales.

The Massachusetts metros are smaller, more affordable places that might make sense for those who work locally or are commuting less to larger, more expensive cities like Boston.

“As people have more remote work, they are willing to live farther away from the office,” says Hale.

The wild card in these top market predictions is mortgage rates. If rates shoot back up again or refuse to retreat to the mid-6% range, many California markets might not see the price and sales growth that Realtor.com has anticipated.

“Seeing mortgage rates come back will be enough to kick-start buyer demand,” says Hale.

November median home list price: $200,000 Forecasted 2024 home sales price change: 8.3% Forecasted 2024 home sales change: 14%

When most folks think about America’s top real estate markets, Toledo might not be their first pick. The Rust Belt city, about an hour southwest of Detroit on the banks of Lake Erie, has seen its share of troubles over the past few decades.

However, the Toledo housing market has remained largely balanced over the past few crazy years. Prices have stayed low, at less than half of the national median price of $420,000 in November.

“It’s less prone to the wild swings we’ve seen in other markets,” says Hale. “The highs weren’t as high and the lows weren’t as low—so that’s one of the reasons they’re going to start to recover first.”

There has been an influx of new buyers in search of affordable homes here, says local real estate agent Rick Turner, of Key Realty. There have also been plenty of investors buying fixer-uppers, renovating them, and then renting out those properties, although they’ve been pulling back a bit recently.

“We’re seeing fewer people who are applying for mortgages right now,” Turner says.

Those looking for entry-level homes in the suburbs can find them in the $250,000 to $300,000 range in places such as Sylvania, OH, and Holland, OH. Buyers searching within the city limits can still score a starter home for about $160,000.

November median home list price: $1,037,000 Forecasted 2024 home sales price change: 3.3% Forecasted 2024 home sales change: 18%

About an hour north of Los Angeles on the coast is Oxnard, an agricultural area known for its picturesque beaches, which include the communities of Thousand Oaks and Ventura.

The area is a cheaper alternative to Los Angeles, where homes have a $1.15 million median price tag—but that gap is closing quickly. List prices in the metro were up 22% in October compared with a year earlier, and homes are selling quicker than in 2022.

November median home list price: $239,000 Forecasted 2024 home sales price change: 10.4% Forecasted 2024 home sales change: 6.2%

Rochester has emerged as a real estate destination thanks to the area’s low home prices and scenic location on Lake Ontario, upstate in New York on the Canadian border. The metro has become a stalwart of the Realtor.com hottest markets list since 2022.

The Rust Belt city, the headquarters of former corporate titan Kodak, struggled over the decades but was awarded $10 million last year for revitalization projects downtown.

There is this three-bedroom, two-bathroom Colonial on more than an acre of land for just under $250,000. Buyers can also snap up this recently renovated three-bedroom, 1.5-bath house for nearly $175,000.

November median home list price: $995,000 Forecasted 2024 home sales price change: 5.4% Forecasted 2024 home sales change: 11%

The inclusion of San Diego on this list might be a head-scratcher. The desirable Southern California city, close to the U.S.-Mexico border, is renowned for its warm weather, miles of beautiful beaches, and the San Diego Zoo.

The metro was smacked hard by surging mortgage rates, which, along with the high home prices, made the area financially untenable for many buyers. Many home sellers were forced to slash their prices and homes sat on the market for longer until the market began turning around this year.

Mortgage broker Julie Aragon, of Aragon Lending, is seeing buyers trade Los Angeles for San Diego, where they can find larger homes in good school districts for less money.

“The bigger houses, there is still a lot of demand for those,” says Aragon.

November median home list price: $585,000 Forecasted 2024 home sales price change: 2% Forecasted 2024 home sales change: 13.8%

Riverside, an area known for its citrus groves about an hour inland from Los Angeles, continues to attract homebuyers from pricier parts of the state. But there is little for them to purchase.

“Our issue this year has been lack of properties put on the market,” says real estate broker Doug Shepherd, of Better Homes and Gardens Real Estate Champions. “No one is selling.”

Roughly 50% to 60% of his clients are chasing affordability from Los Angeles, where the median home price is nearly double that of Riverside, and other areas in Southern California.

“Even at these interest rates, we’re still affordable” to these buyers, Shepherd says. “If we can put more homes on the market, we’ll have more sales. Demand is there.”

November median home list price: $385,000 Forecasted 2024 home sales price change: 2.3% Forecasted 2024 home sales change: 13.4%

Bakersfield is another agricultural area that’s been catching the interest of Los Angelenos as well as remote workers seeking more affordable real estate. The city is inland, about two hours north of the larger city.

“Affordability has always been the biggest draw,” says real estate agent William Gordon, of the Gordon Team Realty. As mortgage rates have dipped recently into the lower 7% range, he’s seen a slight uptick in housing market activity.

“I do see a pretty strong spring coming as long as rates keep dropping,” he adds.

November median home list price: $350,000 Forecasted 2024 home sales price change: 4.2% Forecasted 2024 home sales change: 10.5%

Springfield might be an unusual pick for a national top markets list. But this city, the birthplace of beloved author Dr. Seuss, is luring homebuyers with its affordable home prices and low unemployment.

The metro is about 90 minutes west of Boston on the Connecticut River, with home prices less than half of the larger metro’s median of $837,000, according to Realtor.com list price data in October. And that’s after home prices have steadily risen in the Springfield area since mid-2022.

November median home list price: $475,000 Forecasted 2024 home sales price change: 4.8% Forecasted 2024 home sales change: 9.1%

Similar to Springfield, Worcester has long been a cheaper alternative to Boston. The larger city is only about an hour’s drive to the east.

However, the additional demand for homes in the Worcester area has pushed median home list prices up 42% in just four years, according to Realtor.com October data. And that’s still a major bargain compared with Boston’s prices. That helps to explain why the metro was also named one of the top markets of 2023 by Realtor.com.

The buyers braving the Worcester market are a mix of Bostonians, investors, and locals who can afford the higher prices and mortgage rates, says real estate broker Nick McNeil, of McNeil Real Estate.

“The market obviously is hot, but it is cooling down,” he says. That’s due to today’s buyers facing expensive, monthly mortgage payments and a lack of homes for sale. “I’ve got 20 people here I could probably call and we could list their house tomorrow. But then they’ve got nowhere to go.”

If rates dip into the 6% range, as Realtor.com economists forecast, many sellers and buyers will be nudged off the sidelines, McNeil says. That additional competition will heat the market, pushing prices up even more.

November median home list price: $390,000 Forecasted 2024 home sales price change: 7.2% Forecasted 2024 home sales change: 6.1%

Known for its brewery scene and role in producing office furniture (something the city touts), Grand Rapids is another city that’s seen high home price growth during the COVID-19 pandemic. And prices in Grand Rapids, just east of Lake Michigan, keep notching up.

However, the pervasive lack of homes is stymying the market.

“There are still plenty of people who would purchase if there were homes available,” says real estate broker Steve Volkers, of Five Star Real Estate. “That’s more the issue than the interest rates.”

There are still people moving into the area, many of whom are baby boomers wanting to be closer to family or folks moving in from the other side of the state.

“Before they could buy a lot bigger of a house because interest rates were low,” says Volkers. “But now, they’re just adjusting and finding something within their … budget because they still want to be homeowners.”

November median home list price: $1,150,000 Forecasted 2024 home sales price change: 3.5% Forecasted 2024 home sales change: 9.2%

The Los Angeles housing market took a beating as mortgage rates spiked. Prices slipped or grew very modestly, homes took longer to sell, and many sellers had to cut prices.

However, the market has been rebounding in recent months.

“A lot of our clients are just realizing that, after a year and a half of [higher mortgage rates], these are the rates,” says mortgage broker Aragon.

The problem: There aren’t enough homes to go around. Once rates fall, Aragon anticipates more buyers will jump into the market and the bidding wars will ratchet up.

“It’s going to get more competitive,” she says. “I expect prices to go up a lot.”

Clare Trapasso is the executive news editor of Realtor.com. She was previously a reporter for the Associated Press, the New York Daily News, and a Financial Times publication. She also taught journalism courses at several New York City colleges. Email clare.trapasso@realtor.com or follow @claretrap on X (formerly Twitter).

http://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.png00Phil Whiteheadhttp://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.pngPhil Whitehead2023-12-19 16:35:132023-12-19 16:36:11The Top 10 Real Estate Markets of 2024: You’ll Never Guess Which Ones Made the Cut

It’s an increasingly fraught question, and the answer might depend on who’s being asked.

Some real estate experts believe home prices are well above what they should be and expect them to begin coming down. Others think the high prices make sense given how many people are still in the market looking for properties, despite mortgage rates nearing 8%.

“If you look at how much income homebuyers are putting toward their housing payment, if the number is not the highest ever, it’s really darn close,” says Realtor.com® Chief Economist Danielle Hale.

No one wants to buy a home at the peak of the market—and then watch the home value trickle down.

Homes in 98 of the 100 largest housing markets are selling above their long-term prices, which indicates that they are overvalued, according to an August analysis from Florida Atlantic University and Florida International University researchers. Only two markets had homes selling at a discount.

Nine of the top 10 markets where homes were priced the highest above historical norms were in the South, with seven in Florida, according to the analysis.

“The Sun Belt states are the most overvalued,” says Ken H. Johnson, a real estate economist at Florida Atlantic University in Boca Raton.

However, not everyone believes home prices are out of whack.

One thing most observers agree on: It’s the housing shortage that has kept prices high. Since there aren’t enough properties to go around for all of those aging into prime homebuying years, buyers have been trying to outdo one another with higher and higher offers to win bidding wars.

It happens in artwork, in commodities, in precious metals—and certainly in housing: The rarer, and more desirable, something is, the more valuable it is often considered to be.

“Yes, we’re in an affordability crisis,” says Devyn Bachman, senior vice president of research at the real estate consulting firm John Burns Research and Consulting. But “we have so much demand in the market, I don’t know that you can argue housing is overvalued.”

Fears of buying at the top of the market

It’s nearly impossible to perfectly time investments in the stock market. That is also true in real estate. No one wants to risk buying shortly before a major price correction.

That’s why some buyers who can afford the steep price tags at today’s high mortgage rates might decide to wait.

“There’s always this looming fear that they’re buying at the wrong time or they’re buying at the top of the market,” says Ali Wolf, chief economist of the builder consultancy Zonda. “We thought the peak was last year; we thought the peak was the year before.”

The problem is that it’s often impossible to figure out if the market has peaked until well after the fact. Many thought the market had peaked earlier this year when prices began to dip on a year-over-year basis, but then they started creeping up again.

“If someone is buying now because they want to lock in their interest rate, live in a certain neighborhood, get in a certain school district, and they’re planning to live there at least five years, I wouldn’t be as concerned about trying to time the market,” says Wolf.

Mortgage rates will determine whether home prices rise or fall

If rates come back down, that could lure more buyers back into the market and prices could rise more steeply again.

(David Paul Morris/Bloomberg via Getty Images)

Home prices aren’t sitting by themselves on an island. Mortgage rates and incomes also play a large part in whether real estate is overvalued.

It’s simple math. If everyone in America made at least $1 million a year, September’s median home list price of $430,000 wouldn’t seem so extra. Similarly, if mortgage rates were below 3%, then today’s prices would also be a lot more palatable.

“Two years ago, home prices were [also] high, but interest rates were low and most markets were considered fairly valued,” says Wolf. “The reason that’s changed today is mortgage rates have more than doubled.”

If mortgage rates keep climbing, home prices could fall. There is a limit to how much buyers can afford to spend each month on housing.

“It’s definitely more risky [to buy] today because of the high interest rates,” says Wolf. “If someone is buying now because they think their home [will be] up in value one year from now, I wouldn’t guarantee it.”

But if rates come back down, that could lure more buyers back into the market and prices could rise more steeply again.

“If mortgage rates drop, then maybe your asset isn’t overvalued,” says Bachman.

Will home prices crash?

Even if home prices are overvalued, most real estate experts don’t expect another housing crash to correct them.

“It’s certainly possible that home prices could fall from recent highs. It’s also possible they could still go up,” says Hale. “One year ago, everyone was predicting that the sky would fall in real estate—and that hasn’t happened in most markets.”

Unlike during the Great Recession, there are more buyers today than there are homes for sale. That shortage is expected to put a floor under prices, keeping them more elevated than many buyers would prefer.

Lenders have also tightened underwriting so that only more qualified borrowers get loans. That’s likely to prevent another wave of foreclosures, flooding the market with cheap real estate.

“There is going to be some adjustment. It could be that prices fall, it could be that incomes grow to catch up, it could be that mortgage rates come back down,” says Hale. “Or each of these three things could contribute a little bit over time until we gradually get back to housing taking up a more normal share of income.”

She also notes that housing markets rarely bottom out quickly. During the Great Recession, it took about four years for prices to fall to their nadir.

Even if prices did correct, most homeowners have enough equity in their homes to not find themselves underwater on their mortgages, says Hale.

The exceptions are recent homeowners who haven’t had as much time to pay down their balances or benefit from the steep price increases of the past few years. There is also a greater risk for those who purchased their homes with low down payments; they could be in the uncomfortable position of owing more than their homes are worth if prices came down by double digits.

But over time, the housing market generally rebounds and prices begin rising again. Homeowners just have to hold on. Even if the housing market is overvalued, people who need a home will still buy.

“It’s very clear that housing is expensive right now,” says Hale. But “even if housing is overvalued, it will make sense for people to buy homes.”Clare Trapasso is the executive news editor of Realtor.com. She was previously a reporter for the Associated Press, the New York Daily News, and a Financial Times publication. She also taught journalism courses at several New York City colleges. Email clare.trapasso@realtor.com or follow @claretrap on X (formerly Twitter).

http://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.png00Phil Whiteheadhttp://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.pngPhil Whitehead2023-12-19 07:13:232023-12-19 07:13:25Is the Housing Market Overvalued? What Buyers Need To Know

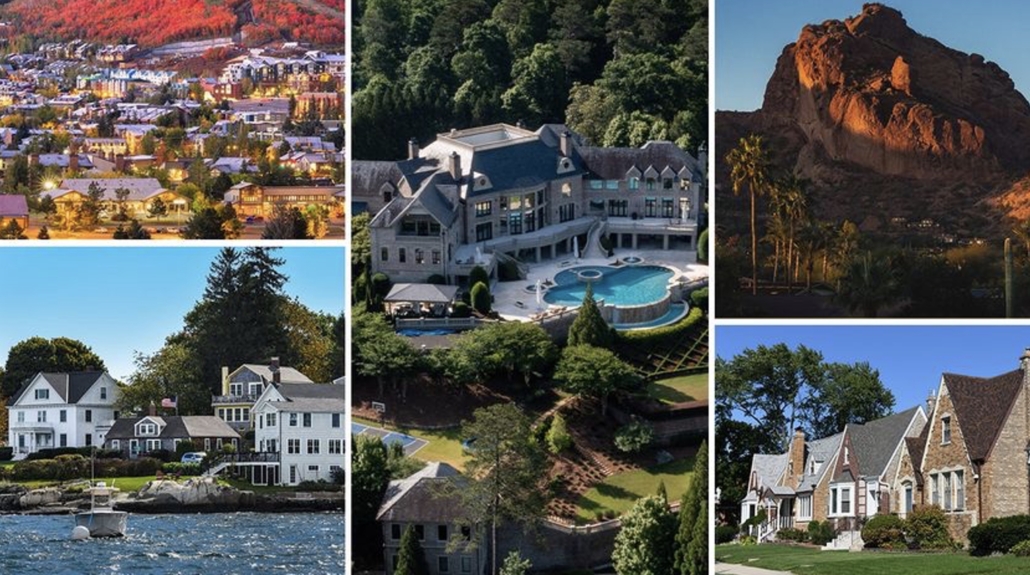

There’s a quiet but undeniable thrill that comes from browsing photos and taking virtual tours of the most opulent properties in America. It’s a hobby less about browsing for a home and more about the fantasy—unless you’re in the richest 1% and could easily afford one of these lavish abodes.

But rest assured, there’s nothing wrong with poring over photos of luxury homes that you’ll buy when you win the Powerball/sell that screenplay you’ve been working on since high school/launch the next great tech startup. We get it! The data team at Realtor.com® found all of the poshest neighborhoods in the nation for your perusing pleasure.

We found the priciest ZIP code in every state with the highest median home list price in October, excluding areas with fewer than 25 listings. Many are upscale vacation destinations popular with the uber-wealthy.

It’s a coast-to-coast tour of extravagance, from breezy Hawaiian beaches and the dramatic shorelines of Maine to the rugged terrain of Colorado’s San Juan Mountains and Arizona’s sun-baked Sonoran Desert.

So, whether you’re in the market for a mansion or only musing, take a tour of some of the most extraordinary real estate in America.

http://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.png00Phil Whiteheadhttp://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.pngPhil Whitehead2023-12-02 12:37:582023-12-02 12:38:00Laps of Luxury: The Priciest Neighborhoods To Buy a Home—State by State

It was never the avocado toast and cappuccino. The joke of millennials not buying homes in favor of overpriced coffee is an entrenched myth. It is important to break down what is really going on, what the numbers are and what the measures mean.

Looking at the U.S. population by age group (see chart to right), one can see that millennials are the largest generation of Americans ever. The red line represents the age of 36, which is the median age of today’s first-time homebuyers. This is the oldest seen since the National Association of REALTORS® (NAR) started collecting data on the age of buyers in 1981. Traditionally, the data has shown that the typical first-time buyer was between the ages of 28 and 33. (The second red line, at age 59, marks the median age of repeat buyers.)

At the same time that the median age of first-time buyers has jumped, their share of the market is at historic lows. In 2023, first-time buyers made up just 26% of the primary residence market, while the historical average is 40%, dating back to 1981.

Low housing inventory, which has averaged nearly 1 million units in the market, is a factor. Today’s higher interest rates are pricing some consumers out. In many areas of the country, home prices are rising. Areas where home prices have softened tend to be where multiple bids pushed up prices throughout the pandemic.

Even among successful first-time buyers, multiple debts made it difficult for them to save for a down payment. Among those who said saving for a down payment was difficult, the most-cited hurdles were high rent (40%), car loan (39%), credit card debt (38%), student loans (35%) and childcare costs (19%). The recent softening in rental prices will be a welcome relief to some moving forward. Twenty-seven percent of successful first-time buyers in 2022 skipped rent and moved directly from a family member’s home into homeownership. This is the highest share recorded by NAR since 1989.

It’s worth noting that student debt was cited as one of the top four reasons buyers had trouble saving for a down payment at a time when student debt payments were paused for many loan holders. Even with the pandemic pause, student loan holders may have been reticent to take out a mortgage, knowing payments could resume. A smaller share of buyers cited childcare costs, but for those who are paying for childcare, the cost can be daunting. In fact, it has increased 220% since 1990, and was $883 per month on average for one child in 2021.

So with that bleak picture, where is the homeownership rate for those under 35? Census data provides a consistent reading of the homeownership rate by age, though this does not match directly to generational trends. When looking at the Census homeownership-rate data, there have been positive reports that the rate improved for those under 35. This is true. From 2021 to 2022, the homeownership rate did improve.

However, if one compares the homeownership rate from 1982 to today, and then separates the data by generation, it tells a less positive story. For baby boomers and Gen Xers, the average homeownership rate for those under 35 was 39.7%. There has yet to be a year that millennials have reached that number.

That leads to the last chart (see below). Even though millennials are the largest adult generation in the U.S. today, they represented a shrinking share of the market last year. This is at odds with what one would expect. That’s because most millennials have reached an age where a home purchase, or at least household formation, is typical. Yet, this year’s data shows that baby boomers overtook millennials as a share of the market. One clear reason is that older buyers have saved money and benefited from home-price appreciation, giving them the ability to pay all cash for a home purchase. With 51% of older boomers and 32% of younger boomers paying cash for their most recent purchase, boomers are the likely winner if there is a bidding war on a home.

Designing the perfect roof for your home is more than just about protection. It’s about creating a harmonious blend of style, color, and function that complements your overall home exterior. As a homeowner, ensuring your roof design matches your home’s aesthetic can significantly enhance curb appeal, potentially increasing property value and setting your home apart in the neighborhood. Not to mention it’ll make you love your house more! This blog post will delve into the importance of a cohesive roof and exterior design, how to identify your home’s architectural style, choose the right roof material, balance functionality with aesthetics and find inspiration from trending roof designs. So, whether you’re building a new home or simply want to give your existing roof a makeover, these tips and insights will guide you through the process of designing and customizing your roof to ensure it perfectly matches your home exterior.

Understanding the Importance of a Cohesive Roof and Exterior Design

A well-thought-out roof design not only adds a protective layer to your home but also amplifies its aesthetic appeal. The right roof, in harmony with your home’s exterior, can significantly elevate your home’s curb appeal, making it stand out in the neighborhood. However, creating a cohesive roof and exterior design requires careful consideration of materials, colors, and architectural style. The choice of roof design should resonate with the architectural style of your home, whether it’s modern, colonial or craftsman. Moreover, the color and material of your roof should complement, not clash with, the exterior finish of your house, giving it a unified appearance that you’ll love to look at.

Identifying Your Home’s Architectural Style and Its Impact

Identifying the architectural style of your home is the first step in determining the right roof design. For instance, a modern home might look best with a sleek, metal roof, while a craftsman-style home might be better suited for a traditional shingle roof. Colonial-style homes often pair beautifully with slate roofs, offering an elegant and timeless appeal. Once the architectural style is identified, it becomes easier to narrow down suitable materials and colors that will complement the house’s exterior. Remember, the goal is to create a harmonious blend between the roof and the rest of the house’s exterior.

Choosing the Right Roofing Material to Complement Your Exterior

The choice of roofing material is a critical aspect of your roof design as it directly influences the overall aesthetic and durability of your roof. Asphalt shingles, for example, are versatile and can suit a variety of home styles due to their wide range of colors and designs. On the other hand, metal roofing, with its modern and slick appearance, can be ideal for contemporary homes. If you’re aiming for a more luxurious appeal, slate or tile roofing could be the right choice, especially with classical or Mediterranean-style homes. Regardless of the material you choose, ensure it harmonizes with your home’s exterior finish, trim and architectural style.

Balancing Functionality and Aesthetics

While designing your roof, it’s essential to strike a balance between functionality and aesthetics. A visually appealing roof is no good if it doesn’t protect your home effectively, nor is a sturdy, leak-proof roof that jars with your home’s exterior. Consider factors like climate, exposure to extreme weather and maintenance requirements when choosing roofing material and design. For instance, a beautiful wooden roof might not be the best choice if you live in an area with heavy rainfall. Ultimately, a well-designed roof should not only enhance your home’s beauty but also offer optimal protection against the elements.

Finding Trends in Roof Designs to Enhance Your Home’s Curb Appeal

In the world of roofing, there are several trends that homeowners can consider to enhance their home’s curb appeal. Solar roofing, for instance, has gained popularity not just for its sleek, modern appearance, but also for its energy-efficient advantages. Green roofs, adorned with vegetation, offer a unique, eco-friendly aesthetic, while also providing excellent insulation. For a more traditional appeal, gable roofs with contrasting colors are making a comeback, providing the perfect blend of classic charm and modern style. Finally, bold colors for roofs are trending, adding a dramatic pop of color which can elevate the overall exterior of the house.

In conclusion, designing a roof that comports with your home’s exterior is an art that requires a keen understanding of architectural styles, roofing materials and current trends. It’s all about melding aesthetics with functionality, ensuring your roof not only protects your home but also enhances its curb appeal. This is no small task to undertake on your own. Designing and building a roof is a complex process that demands professional expertise. Hiring professionals can save you from potential pitfalls and guide you in making the best choices for your home. They can help you navigate the vast array of materials and designs, and ensure your roof is installed to the highest standards. Your roof is a significant investment and a fundamental part of your home’s identity. So, make sure it’s in the right hands and let the professionals help you create a roof that you can be proud of and that perfectly matches your home’s exterior.

Rachelle Wilber is a freelance writer living in the San Diego, California area. She graduated from San Diego State University with her Bachelor’s Degree in Journalism and Media Studies. She tries to find an interest in all topics and themes, which prompts her writing. When she isn’t on her porch writing in the sun, you can find her shopping, at the beach, or at the gym. Follow her on twitter: @RachelleWilber

http://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.png00Phil Whiteheadhttp://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.pngPhil Whitehead2023-11-28 18:25:052023-11-28 18:25:12Roof Design Tips To Ensure It Matches Your Home Exterior

After rising for seven weeks straight, mortgage rates have finally hit a speed bump, falling to 7.76 % on average for a 30-year fixed-rate mortgage as of Nov. 2, according to Freddie Mac.

This hiccup comes on the heels of the Federal Reserve’s announcement on Nov. 1 to not raise benchmark interest rates in its ongoing fight against inflation.

“The Federal Reserve again decided not to raise interest rates,” said Sam Khater, Freddie Mac’s chief economist, “but have not ruled out a hike before year-end.”

While any drop in mortgage rates is welcome news for homebuyers, last week’s rate of 7.79% still hovers at a high not seen since 2000.

“The 23-year high in mortgage rates follows all-time lows reached just three years ago,” says Danielle Hale, chief economist for Realtor.com® in her analysis. This steep rise also “highlights the effect that financing costs have on the housing market–a particularly rate-sensitive sector of the economy.”

We’ll break down what all the latest real estate data means for buyers and sellers in this installment of “How’s the Housing Market This Week?”

Home prices head higher

In addition to high mortgage rates, homebuyers must contend with high home prices, which hovered at a nationwide median of $425,000 in October.

And for the week ending Oct. 28, home prices rose by 1.2%—the highest in 25 weeks—compared with the same time last year.

“Sustained prices can be attributed to the persistently low inventory of existing homes for sale,” says Realtor.com data scientist Sabrina Speianu in her most recent analysis. “Soft demand still continues to outpace the limited supply of homes.”

Home prices, in general, have been on a reasonably even keel since mid-July. And while prices aren’t falling, the market can find a tiny bit of solace in that they aren’t rising dramatically, either.

The intractable inventory issue

The not-so-secret ingredient the housing market needs to get cooking? Lots more homes for sale.

Nationwide, the number of homes for sale shrank by 1% for the week ending Oct. 28 compared with this same week last year, marking the 19th consecutive week of dwindling listings.

For anyone wondering just how low inventory levels are from a historical perspective, consider that the number of homes for sale is 41.8% below typical pre-COVID-19 levels.

“The usual seasonal buildup in inventory that makes this time of year favorable for buyers is underway, but from a longer-term macroeconomic perspective, housing remains undersupplied,” explains Speianu.

An abrupt reversal in new listings

But as days grow shorter, here’s a sliver of light: New listings were up by 5.6% for the week ending Oct. 28 from one year ago.

“Since mid-2022, new listings have registered lower than prior-year levels, as the mortgage rate lock-in effect freezes homeowners with low-rate existing mortgages in place,” says Speianu. “This past week, the trend abruptly reversed.”

But whether the trend will continue remains to be seen.

“While newly listed homes this past week exceeded the figures from the same week last year, the overall pace of listing activity still severely lags behind the levels seen before the pandemic,” says Speianu.

Homebuyers still need to act fast

Buyers who do find a great property in the meager home haystack don’t have much time to linger over a pro and con list.

For the week ending Oct. 28, homes spent one less day on the market compared with last year. (The average time on the market for a typical home was 50 days in October, more than two weeks shorter than before the COVID-19 pandemic.)

“The gap in time on the market narrowed over the last few months as buyers competed over fewer homes,” says Speianu. “This fall, the time a typical home spends on the market is growing much more slowly than is typical for this season.”

http://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.png00Phil Whiteheadhttp://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.pngPhil Whitehead2023-11-23 12:53:052023-11-23 12:53:44Mortgage Rates Have Just Abruptly Reversed Course—Will It Last?

With mortgage interest rates hitting record highs not seen in decades and quickly approaching 8%, many might wonder: How much more does it actually cost to buy a house today?

According to a new report by Realtor.com®, the monthly cost of financing 80% of a typical home jumped by $166 in October compared with this same month last year.

That’s “a new record, on top of what was already the highest amount since Realtor.com began tracking this data in mid-2016,” says Realtor.com Chief Economist Danielle Hale.

Do the math, and this means that today’s homebuyers must cough up $2,405 per month for the privilege of owning a house. And in order to comfortably afford those mortgage payments, a homebuyer would need an annual salary of $119,500—nearly double the actual median household income of $64,240.

In other words, the typical American makes only about half as much as they need to afford a home today.

The latest trends in home prices

Sky-high mortgage rates aren’t the only metric keeping real estate in a prolonged affordability crunch.

Despite high mortgage rates, home prices aren’t budging much, with the median list price in October hovering at $425,000. That number has remained more or less stable compared with this same time last year.

“Listing prices have been buoyed by scarce inventory,” says Hale.

The one upside for buyers is that home prices are declining seasonally, down from $430,000 in September. They’re also down from their all-time high of $450,000, in June 2022.

Why low housing inventory keeps prices higher than usual

The overall number of homes for sale in the U.S. sank by 2% in October compared with this same month last year. That percentage might not seem dramatic at first glance, but this scarcity of listings is downright shocking when compared with pre-COVID-19 levels from 2017 to 2019, which boasted 42.4% more homes for sale.

As for fresh listings, those were also down by 3.2% in October, compared with last year.

A growing number of buyers are turning to purchasing new construction.

“New-home sales have been increasing,” says Hale. However, “construction activity isn’t elevated enough to fully bridge the low inventory gap.”

The housing inventory outlook

So, when can buyers expect to see a substantial increase in new listings and active inventory overall?

“That is the trillion-dollar question in housing right now,” says Hale, who expects it will be “quite a bit longer before buyers can see a large increase in new listings and the number of homes for sale.”

The delay all comes down to sellers who feel “locked in” to their much lower mortgage rates of just a few years earlier.

“Because so many homeowners either purchased their home or refinanced their mortgage during the pandemic period, when interest rates were low, their homes are likely still a very good fit for their needs and quite affordable,” explains Hale. “Especially relative to the cost of buying at today’s mortgage rates.”

Motivated buyers are pouncing

In a surprise twist, the cruel combination of steep mortgage rates, high home prices, and scant listings doesn’t mean buyers can take their time making an offer. Instead, the opposite is true: Today’s buyers must act relatively swiftly when they spot a great home.

“Homes spent 50 days on the market, which is one day shorter than last year,” says Hale.

In fact, the average home spent 16 fewer days on the market than the pre-pandemic average for October from 2017 to 2019.

And although time on the market typically lengthens as we approach the holidays, “Time on market is rising more slowly this year than is typical during the fall season, as still-limited supply spurs homebuyers to act quickly and newly listed homes make up a greater share of low remaining inventory,” says Hale.

Where home prices are softening

The Federal Reserve held rates steady at its meeting on Wednesday, but it left open the possibility that more rate hikes could occur if inflation doesn’t keep coming down.

Until mortgage rates subside, today’s real estate market can be best described as a financial bully, grabbing homebuyers by the ankles and shaking every last nickel out of their housing budget.

Yet all real estate is local, and America’s 50 largest housing market metros do show some pockets of hope for homebuyers.

In the bad news column for buyers: In October, real estate listings in the top 50 metros dropped 6.7% compared with the same month last year, while the collective inventory across these areas is now 38.4% below pre-pandemic levels. (Metros include the central city, surrounding towns, suburbs, and smaller urban areas.)

But in the good news column? While overall home price reductions were still below last year’s levels in all four regions of the U.S., some of these metros were seeing sellers slash prices.

Indeed, “13 of the 50 large metros saw the share of price reductions increase compared to last October, predominantly in the South and Midwest,” says Hale.

“While lower than last year, the share of price reductions rising could signal a softness in prices in the coming months,” concludes Hale.

Margaret Heidenry is a writer living in Brooklyn, NY. Her work has appeared in the New York Times Magazine, Vanity Fair, and Boston Magazine.

http://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.png00Phil Whiteheadhttp://genebrazzell.com/wp-content/uploads/2017/02/Gene-Brazzell-MR-Realty-Real-Estate-Lexington-SC-300x139.pngPhil Whitehead2023-11-20 19:54:562023-11-20 19:56:59Housing Costs Have Just Hit a ‘New Record’: Here’s What That Adds Up to in Dollars and Cents